Bunching charitable donations is a tax planning strategy that may help some 1099 professionals group multiple years of giving into one tax year so they can potentially benefit from itemized deductions.

For self-employed professionals, charitable giving should not be reviewed in isolation. It should fit into the larger tax picture, including income, estimated tax payments, business deductions, retirement contributions, and year-end planning.

This can matter for high-income contractors, CRNAs, locum tenens providers, nurse practitioners, physician assistants, and other 1099 professionals who want to give intentionally while keeping their tax records organized.

What Does Bunching Charitable Donations Mean?

Bunching charitable donations means grouping multiple years of planned charitable gifts into one tax year.

Instead of giving the same amount every year, a taxpayer may donate more in one year and less in the following year. The goal is to increase itemized deductions in the higher-giving year.

This strategy is usually considered when regular annual giving does not push itemized deductions above the standard deduction. In that case, charitable donation bunching may help a taxpayer review whether itemizing makes sense for a specific year.

Why the Standard Deduction Matters for Charitable Giving

Many taxpayers take the standard deduction instead of itemizing deductions.

If a taxpayer takes the standard deduction, regular charitable donations may not always create an additional itemized deduction benefit. Beginning in tax year 2026, the IRS notes that some non-itemizers may deduct a limited amount of certain cash charitable contributions, but larger charitable deduction planning still often depends on whether itemized deductions exceed the standard deduction.

Bunching may help when charitable contributions, mortgage interest, state and local taxes, and other itemized deductions together exceed the standard deduction.

The IRS explains qualified organizations, deductible contributions, contribution limits, records, and reporting rules in its IRS charitable contribution guidance.

How Bunching Charitable Donations May Work in 2026

A taxpayer who normally gives smaller amounts each year may choose to make two or more years’ worth of donations in one tax year.

In the bunching year, the goal is to make itemized deductions higher than the standard deduction. This matters in 2026 because itemized charitable deductions may also need to exceed the 0.5% AGI floor before they create a deduction benefit. Bunching can make it easier to clear both the AGI floor and the standard deduction in the same year.

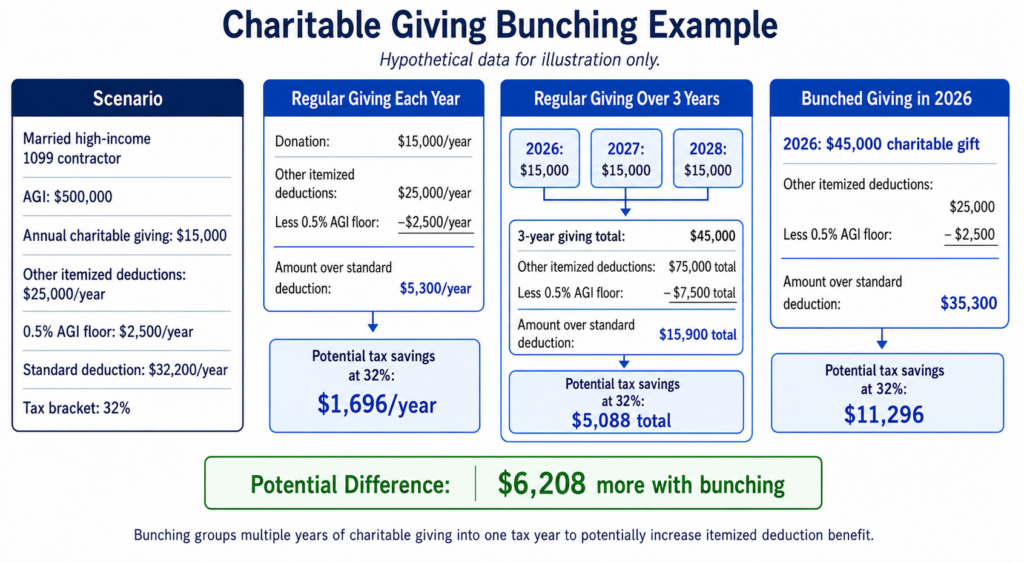

Example Scenario:

Assume a married high-income1099 contractor has an AGI of $500,000, gives $15,000 per year to qualified charities, and has $25,000 in other itemized deductions each year. The 0.5% AGI floor is $2,500, and the standard deduction for married filing jointly is 32,200.

| Scenario | Donation | Other Itemized Deductions | Less 0.5% AGI floor | Amount Over Standard Deduction | Potential Tax Savings at 32% |

| Regular giving each year | $15,000/year | $25,000/year | ($2,500/year) | $5,300/year | $1,696/year |

| Regular giving over 3 years | $45,000 total | $75,000 total | ($7,500 total) | $15,900 total | $5,088 total |

| Bunched giving in 2026 | $45,000 in 2026 | $25,000 in 2026 | ($2,500) | $35,300 | $11,296 |

In this simplified example, bunching creates a larger potential deduction benefit in 2026 because the taxpayer groups three years of charitable giving into one year. The taxpayer may then return to standard deduction in later years if itemizing no longer makes sense. Actual results depend on income, filing status, other deductions, documentation, contribution limits, and current-year tax rules.

What Donations Need to Qualify?

Charitable contributions generally need to go to qualified organizations, and cash and noncash gifts may have different rules. Donations to individuals are generally not treated the same as qualified charitable contributions.

For 1099 professionals, it is also important to separate charitable giving from business deductions. Charitable donations are generally personal itemized deductions reported on Schedule A, not ordinary business expenses on Schedule C.

For business deduction planning, review our 1099 tax deductions list for contractors and our guide to 1099 tax deductions for CRNAs and locum tenens providers.

When Bunching Charitable Donations May Not Make Sense

Bunching charitable donations may not make sense for every taxpayer.

It may not help if the taxpayer does not donate enough to benefit from itemizing. It may also be less useful if cash flow is tight, income is lower than expected, or the taxpayer is unsure whether they will itemize.

The strategy may also create problems if documentation is missing. Without receipts, written acknowledgments, or qualified charity details, the deduction may be harder to support. Because of this, bunching should be reviewed carefully before making a large year-end donation.

How to Review Charitable Giving as Part of 1099 Tax Planning

Start by reviewing year-to-date income, projected tax liability, and estimated tax payments, then review itemized deductions, charitable giving goals, business deductions, and personal deductions separately. This is especially important because charitable donations are usually personal itemized deductions, while business deductions follow different rules.

High-income 1099 professionals may also need to review retirement contributions, state tax planning, and entity strategy. For healthcare contractors, S-Corp tax planning for high-income CRNAs may also be part of the year-end planning conversation.

Accurate bookkeeping for 1099 professionals can make this review easier because income, expenses, reimbursements, and prior estimated payments are already organized.

Work With 1099 Accountant Before Making Year-End Tax Moves

Bunching charitable donations can be useful for some 1099 professionals, but it should fit your full tax picture. Before making a large donation, review your income, estimated taxes, itemized deductions, business expenses, and year-end planning options.

1099 Accountant helps CRNAs, locum tenens providers, nurse practitioners, and self-employed professionals plan around 1099 income, deductions, estimated taxes, and tax strategy.

Schedule a consultation or contact us at (855) 529-1099 before making year-end tax planning decisions.